How Financial Planning Impacts the Purchase of New and Used Cars

Understanding the Connection Between Financial Planning and Car Purchases

When it comes to buying a car, the excitement of choosing a new vehicle can sometimes overshadow the more practical aspects of the purchase. However, effective financial planning is essential to making well-informed decisions that can affect your financial health long after the purchase is made. This process involves several key components that can help ensure you make a purchase that aligns with your budget and long-term financial goals.

Budgeting

Establishing a clear budget is one of the first steps in financial planning for a car purchase. It is vital to consider not only the sticker price of the vehicle but also the ongoing expenses associated with ownership. These include costs such as insurance, fuel, maintenance, and potential repairs. For example, when budgeting, you might discover that a less expensive used car could actually become more costly due to higher maintenance fees, compared to a slightly pricier new car that comes with a warranty. By calculating these additional costs upfront, you can avoid financial strain in the future.

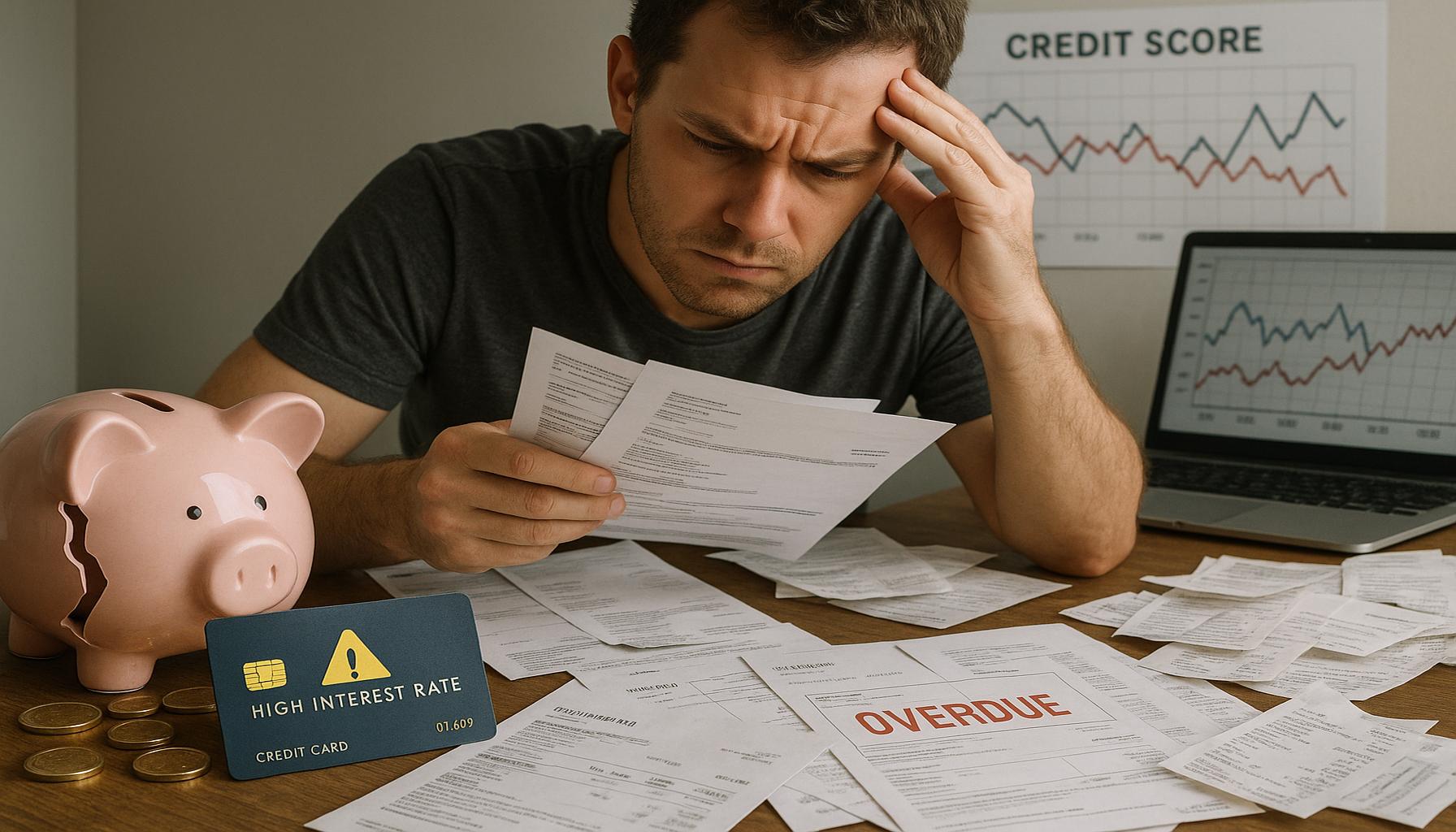

Credit Score

Your credit score plays a pivotal role in the purchasing process. A healthy credit score demonstrates to lenders that you are a responsible borrower, which can lead to more favorable financing options. For instance, a borrower with a score of 760 or higher may qualify for interest rates as low as 3% when financing, while someone with a score below 620 might face rates exceeding 7%. These differences can result in thousands of dollars over the life of a loan. Therefore, it’s wise to check your credit report and address any issues before shopping for a car.

Loan Terms

Understanding various loan terms is also key to securing the best deal on your car purchase. Loans often come with different repayment plans—typically ranging from 36 to 72 months. A shorter loan term tends to mean higher monthly payments, but you pay less interest overall. Conversely, a longer term means lower monthly payments, but you may end up paying more in interest over time. By assessing your budget and financial situation, you can choose a loan structure that balances affordability with the total cost of the vehicle. For example, if your budget allows for higher payments, a 48-month loan might be the best choice for minimizing interest expense.

By focusing on these critical aspects of financial planning, you can navigate the car-buying process confidently and competently. Effective financial planning doesn’t simply help you make smarter choices; it empowers you to enjoy your new or used vehicle without the cloud of unmanageable debt looming over you. Taking the time to budget, understand your credit, and evaluate loan terms can lead to a more satisfying and financially sound vehicle purchase.

DISCOVER MORE: Click here to learn how to apply for the Luxury Mastercard Black

Essential Financial Considerations for Car Buyers

The journey to purchasing a car can be thrilling, but it is important to ground that excitement in a solid financial understanding. Beyond just the initial cost of purchasing a vehicle, there are numerous financial factors to consider. These factors can significantly impact not only your immediate budget but also your long-term financial stability. Here are several essential considerations that every car buyer should take into account:

Down Payment

One of the first financial decisions to make when buying a car is your down payment. This is the amount of money you pay upfront when buying the car, and it significantly influences the amount you will need to finance. A larger down payment can result in lower monthly payments and reduced interest charges over the life of the loan. For example, if you’re buying a $20,000 car and make a 20% down payment of $4,000, you will only finance $16,000. This decreases your total interest liability compared to financing the entire purchase price.

Monthly Payments

Understanding what you can realistically afford each month in terms of monthly payments is crucial. Experts often recommend that your car payment should not exceed 15% of your monthly take-home income. This ensures that you can comfortably manage other expenses, such as housing, food, and savings, without feeling financially cramped. To put this into perspective, if your take-home income is $3,000 a month, then your total car expenses— including your payment, insurance, and maintenance—should be no more than $450.

Insurance Costs

Insurance is another vital part of car ownership that requires careful financial planning. When budgeting for a new or used car, don’t overlook insurance costs. Insurance rates vary based on several factors including the vehicle’s make and model, your age, driving record, and location. For instance, a newer car with advanced safety features may have lower premiums due to less risk of accidents. Conversely, a high-performance sports car may incur significantly higher insurance costs. It’s wise to get insurance quotes before making your final decision on a vehicle to avoid surprises down the road.

Long-term Maintenance

Thinking about the long-term maintenance of a vehicle is just as important as considering its upfront price. New cars typically come with warranties that cover most repair costs in the initial few years of ownership. On the other hand, used cars may require more investment in maintenance and repairs as they age. Issues like timing belt replacements, brake jobs, and tire replacements can add up quickly. Here are some maintenance-related factors to consider:

- Age and mileage of the vehicle

- Previous maintenance records

- Availability of parts and service for the make and model

By building these potential expenses into your financial planning, you can better prepare for the total cost of ownership.

Incorporating these considerations into your financial planning will create a more holistic view of how your car purchase impacts your budget and financial goals. By making informed decisions around your down payment, monthly payments, insurance costs, and long-term maintenance, you can ensure that your car fits comfortably within your financial landscape, allowing you to enjoy your vehicle without worry.

DISCOVER MORE: Click here for all the details

Additional Financial Factors to Navigate When Purchasing a Vehicle

After considering the initial financial factors such as down payment, monthly payments, insurance costs, and long-term maintenance, buyers should also focus on the overall total cost of ownership and the role that financing plays in the purchasing decision. Understanding the broader context of financial implications can empower buyers to make informed decisions.

Total Cost of Ownership

When purchasing a vehicle, it’s crucial to evaluate the total cost of ownership (TCO), which encompasses not just the purchase price, but also other ongoing expenses. This includes fuel, maintenance, repairs, insurance, and even depreciation. For instance, an electric vehicle may have a higher upfront cost but could offer significant savings in fuel and maintenance over time compared to a traditional gas-powered vehicle. To calculate TCO, consider these components:

- Fuel efficiency: Compare miles per gallon (MPG) or electric vehicle range.

- Maintenance costs: Research common issues for specific makes and models.

- Depreciation: New cars typically lose value faster than used cars, affecting resale value later.

By calculating TCO for the cars you’re considering, you’ll have a clearer picture of how much you’ll end up spending throughout the vehicle’s life.

Financing Options

The financing options available to you can greatly impact your purchasing decisions. When exploring loans, consider not only the interest rate but also the duration of the loan. A shorter loan term usually means higher monthly payments, but it can save you a significant amount in interest. For example, if you finance a new car at 5% interest for 60 months versus 72 months, your monthly payment may be higher with the shorter term, but the total interest paid over the life of the loan would be lower. Additionally, shop around for loan terms from banks, credit unions, and dealership financing to find the most favorable options for your situation.

Impact of Credit Score

Another critical element to consider is your credit score. Lenders use credit scores to assess your creditworthiness, which can directly affect your financing options. A higher credit score can qualify you for better interest rates, reducing your monthly payments and overall loan cost. For example, a person with a credit score of 750 may secure a loan at 3% interest, while someone with a score of 600 might face rates upwards of 7%. It’s wise to check your credit report prior to car shopping and take steps to improve your score if necessary, such as paying down existing debts.

Future Financial Goals

Finally, consider how purchasing a vehicle fits into your broader financial goals. Whether it’s saving for a home, retirement, or education, a car should align with your financial plan. Ask yourself whether financing a vehicle fits into your long-term budget and how it may affect your ability to save for other critical goals. For example, if buying a more luxurious new car significantly stretches your budget, it could hinder your ability to make contributions to a retirement account or pay off student loans.

By analyzing the total cost of ownership, understanding financing options, keeping an eye on your credit score, and aligning your car purchase with your future financial goals, you can make a car-buying decision that supports not only your immediate transportation needs but your long-term financial well-being as well.

DISCOVER MORE: Click here to learn how to apply for the Chase Freedom Unlimited credit card

Conclusion

In summary, sound financial planning plays a pivotal role in guiding consumers through the car-buying process, whether they are considering new or used vehicles. By understanding the total cost of ownership, buyers can make choices that are not only affordable in terms of monthly payments but also sustainable over the long term. This evaluation includes ongoing costs such as fuel, maintenance, and depreciation, enabling a more comprehensive view of the financial commitment involved.

Furthermore, the implications of financing options and their connection to your credit score cannot be overstated. Weak credit can lead to higher interest rates, while a strong credit profile can present opportunities for more favorable loan terms. Taking proactive steps to improve your credit can yield significant savings over time.

Finally, it’s essential to align any vehicle purchase with your broader financial goals. Whether you are saving for a home, retirement, or education, a vehicle should be viewed as part of an overarching financial framework. By integrating all these elements into your decision-making process, you ensure that your car purchase is not just a means of transportation, but a smart investment that supports your financial health.

Ultimately, taking the time to thoroughly assess your finances before making a vehicle purchase will empower you to make decisions that balance both immediate needs and future aspirations.